Key Takeaways

- Interest rates are the most powerful external force on real estate values — lower rates increase purchasing power and push prices higher.

- Employment growth drives housing demand; job creation in a market is the strongest leading indicator of price appreciation.

- Demographic trends (millennials entering home-buying years, boomers aging) create predictable long-term demand patterns.

- Government policy shapes real estate through tax incentives, regulation, and mortgage market support.

- Capital market flows affect cap rates and property values — capital abundance compresses returns, capital scarcity creates opportunity.

Real estate does not exist in a vacuum. It is deeply interconnected with interest rates, employment, demographics, government policy, and the broader capital markets. This lesson maps those connections, showing how macroeconomic forces flow through to property values, rents, and investment returns.

Interest Rates and Real Estate Values

Interest rates are arguably the single most powerful external force affecting real estate values. When rates fall, borrowing becomes cheaper, increasing buyer purchasing power and pushing prices higher. When rates rise, the opposite occurs — monthly payments increase, affordability declines, and prices face downward pressure. The Federal Reserve's monetary policy therefore has a direct and significant impact on real estate markets.

Between 2020 and early 2022, the federal funds rate was near zero, and 30-year mortgage rates fell below 3%. This fueled extraordinary home price appreciation, with the S&P/Case-Shiller National Home Price Index rising over 40% in just two years. When the Fed raised rates aggressively in 2022-2023, mortgage rates surpassed 7%, and transaction volumes dropped sharply — though prices proved more resilient than many expected, in part because low inventory constrained supply.

Employment, Demographics, and Demand

Employment growth is the primary driver of housing demand. When an area adds jobs — particularly well-paying jobs — workers migrate in, household formation increases, and demand for both rental and for-sale housing rises. Markets like Austin, Nashville, and Raleigh-Durham demonstrated this dynamic from 2015-2024, with population growth rates 2-3x the national average driven by technology and healthcare sector expansion.

Demographic shifts also shape long-term demand. The millennial generation (born 1981-1996), the largest in U.S. history at approximately 72 million people, entered peak home-buying years in the 2020s, creating sustained demand pressure. Simultaneously, the baby boomer generation's aging is reshaping demand for senior housing, single-story homes, and age-restricted communities. Immigration patterns, household size trends, and urbanization versus suburbanization further influence where and what type of real estate demand grows.

Government Policy and Capital Markets

Government policy affects real estate through taxation, regulation, and direct intervention. The mortgage interest deduction, 1031 exchange provisions, and depreciation allowances all create incentives that influence investment behavior. Zoning laws and building codes determine what can be built and where, directly controlling supply. Government-sponsored enterprises like Fannie Mae and Freddie Mac backstop the residential mortgage market, enabling the 30-year fixed-rate mortgage that is unique to the United States.

Real estate is also linked to capital markets through REITs, commercial mortgage-backed securities (CMBS), and institutional investment flows. When stock markets perform well and investors seek diversification, capital flows into real estate, compressing cap rates and driving prices higher. During credit crunches, capital retreats, liquidity dries up, and distressed opportunities emerge. Understanding these capital market dynamics helps investors anticipate shifts and position accordingly.

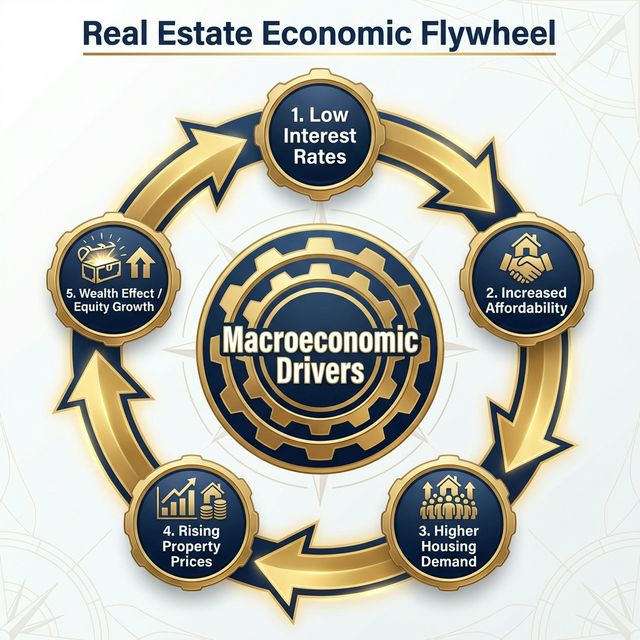

The Real Estate Economic Flywheel

This cycle demonstrates how macroeconomic factors feed into each other. Low interest rates increase affordability, which drives housing demand. This demand pushes property prices up, creating a "wealth effect" for owners, who then have more equity to invest or spend, further stimulating the economy. However, if prices rise too fast, inflation triggers higher interest rates, cooling the cycle.

Cycle diagram showing the feedback loop between Interest Rates, Affordability, Demand, Prices, and Wealth Effect

Key Takeaways

- ✓Interest rates are the most powerful external force on real estate values — lower rates increase purchasing power and push prices higher.

- ✓Employment growth drives housing demand; job creation in a market is the strongest leading indicator of price appreciation.

- ✓Demographic trends (millennials entering home-buying years, boomers aging) create predictable long-term demand patterns.

- ✓Government policy shapes real estate through tax incentives, regulation, and mortgage market support.

- ✓Capital market flows affect cap rates and property values — capital abundance compresses returns, capital scarcity creates opportunity.

Sources

- Federal Reserve Economic Data (FRED)(2025-01-15)

- U.S. Census Bureau — Population Estimates(2025-01-15)

Common Mistakes to Avoid

Investing without understanding the interest rate environment and its direction.

Consequence: Purchasing at low cap rates during a low-rate environment, only to see property values decline when rates rise.

Correction: Monitor Federal Reserve policy and mortgage rate trends. Stress-test every deal against a rate increase of 1-2 percentage points.

Ignoring demographic trends when selecting investment markets.

Consequence: Investing in markets with aging, declining populations that will experience weakening housing demand over time.

Correction: Research population growth, age distribution, and migration trends for every market. Favor markets with growing populations and positive household formation.

Test Your Knowledge

1.What is the single most powerful external force affecting real estate values?

2.Which demographic generation entered peak home-buying years in the 2020s?

3.What is unique about the 30-year fixed-rate mortgage in a global context?